Infinite Banking and Inflation: Understanding Their Impact

In today’s economic landscape, the concepts of Infinite Banking and inflation have become increasingly intertwined as individuals seek effective inflation hedging strategies. As inflation rates soar, many are turning to cash value life insurance options, such as whole life and universal life insurance, to secure their financial future. These policies not only provide essential whole life insurance benefits but also allow policyholders to leverage their cash value for investments, making them a viable tool for financial planning for inflation. By understanding the dynamics of these insurance products, one can potentially mitigate the adverse effects of rising prices and ensure a stable financial footing. With the right approach, Infinite Banking can serve as a strategic response to inflationary pressures, offering both protection and growth opportunities.

In the face of rising costs and economic uncertainty, individuals are increasingly exploring alternative financial strategies, particularly those involving self-banking systems and inflation protection. The idea of using cash value insurance policies, such as permanent life insurance, has gained traction as a means to not only secure life coverage but also to build a financial reservoir. These products offer a dual benefit: they provide a safety net while simultaneously acting as an asset that can grow over time, thus serving as a buffer against inflation. As people seek ways to enhance their financial resilience, understanding how these innovative insurance solutions work can be crucial. This exploration into self-financing and asset accumulation presents a compelling narrative for anyone looking to safeguard their wealth amidst economic fluctuations.

Understanding Inflation and Its Impact on Personal Finance

Inflation is an economic phenomenon that affects purchasing power and overall financial stability. As prices rise, consumers find their money buys fewer goods and services, leading to a need for effective inflation hedging strategies. These strategies can range from investing in assets that traditionally outperform inflation, such as real estate or stocks, to utilizing specific financial products like whole life insurance. Understanding how inflation impacts personal finances is crucial for anyone looking to safeguard their savings and maintain their standard of living.

For many, the concept of inflation often brings uncertainty and anxiety about the future. The challenge lies in planning effectively for inflation within financial strategies, ensuring that investments and savings grow at a pace that can counteract rising prices. Financial planning for inflation is about more than just reacting to changes; it involves proactive adjustments to a portfolio that can include a mix of traditional investments and innovative solutions like cash value life insurance, which can provide both security and growth.

Infinite Banking and Inflation: A Controversial Connection

The Infinite Banking concept claims to offer a unique solution to combat inflation by leveraging cash value life insurance policies. Proponents argue that these policies can act as a personal banking system, allowing individuals to borrow against their cash value for investments. However, skeptics point out that while whole life insurance policies can indeed provide a degree of inflation protection, they are not a panacea. The reality is that these products are just one piece of a much larger financial puzzle and should be considered alongside other inflation hedging strategies.

Additionally, the effectiveness of the Infinite Banking concept during periods of high inflation can be debated. While cash value life insurance does have benefits, such as liquidity and potential growth through dividends, it is essential to recognize that it does not inherently shield policyholders from inflation’s effects. Therefore, while Infinite Banking may provide some advantages, relying solely on it to counteract inflation may not be the most prudent approach for comprehensive financial security.

Whole Life Insurance: A Reliable Inflation Hedge

Whole life insurance has long been regarded as a stable financial product that can serve as a hedge against inflation. The cash value component of whole life policies grows over time, often at rates that outpace inflation. This growth is facilitated by the guaranteed interest provided by the insurance company, which can offer policyholders peace of mind during fluctuating economic conditions. Moreover, the ability to access cash value through loans creates a level of liquidity that many traditional savings accounts do not provide.

Moreover, whole life insurance policies can accumulate dividends, which can be reinvested, further enhancing their growth potential. As inflation rises, the ability to tap into a growing cash value can provide policyholders with necessary funds during uncertain financial times. Therefore, while no investment is entirely immune to inflation, whole life insurance can be a practical component of a diversified portfolio aimed at maintaining financial stability.

Universal Life Insurance: Adapting to Inflation Trends

Universal life insurance is another financial product that can offer some protection against inflation, thanks to its flexible nature. Unlike whole life insurance, universal policies allow policyholders to adjust their premiums and death benefits, which can be advantageous in an inflationary environment. This adaptability means that as costs increase, individuals can modify their policies to ensure they still meet their financial goals.

Additionally, universal life insurance policies often have a cash value component that grows based on interest rates, which can be advantageous in times of rising rates, typically associated with inflation. By providing the option to allocate cash value between fixed and indexed accounts, policyholders can potentially benefit from higher returns during inflationary periods. Thus, universal life insurance serves as a dynamic tool for individuals looking to navigate the complexities of inflation.

Cash Value Life Insurance: A Strategic Financial Asset

Cash value life insurance, including both whole life and universal life policies, is an essential component of financial planning for inflation. These products accumulate cash value that can be accessed during times of need, offering a safety net when inflation is at its peak. With the ability to borrow against this cash value, policyholders can utilize their insurance policies as a source of emergency capital without undergoing the hassle of traditional loan processes.

Furthermore, the cash value in these life insurance products is not only protected from market volatility but also has the potential for growth that can outpace inflation. As interest rates rise, the returns on cash value accounts can increase, providing a double benefit during inflationary periods. Hence, integrating cash value life insurance into a financial strategy can enhance overall resilience against inflation.

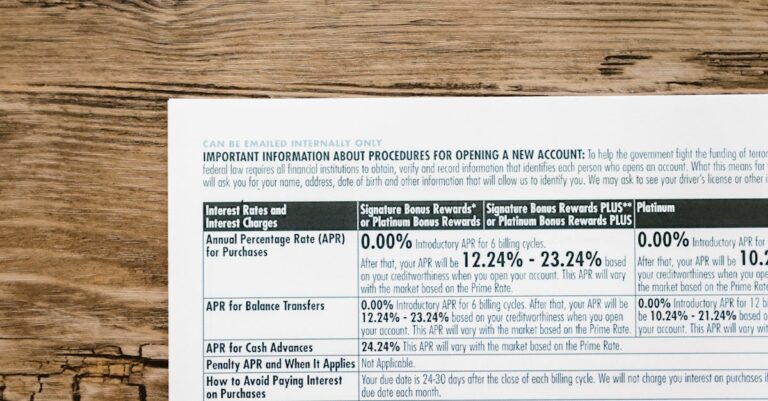

The Role of Interest Rates in Life Insurance Products

Interest rates play a significant role in determining the effectiveness of life insurance products as inflation hedges. As inflation rises, central banks often respond by increasing interest rates to maintain economic stability. This rise in rates can lead to higher returns on cash value life insurance products, which can be particularly beneficial during inflationary times. Investors should keep this dynamic in mind when considering their financial strategies.

Moreover, higher interest rates can also influence policy loans. If an individual borrows against their cash value during high-interest periods, the cost of borrowing may increase. This situation underscores the importance of understanding the terms and conditions of life insurance policies, as well as monitoring broader economic trends, to make informed decisions about leveraging insurance for financial security.

Evaluating Financial Products Amidst Inflationary Pressures

As inflation continues to challenge consumers, evaluating financial products becomes essential. With various options available, including whole life and universal life insurance, individuals must assess which products align with their financial goals and risk tolerance. Understanding the benefits and limitations of each can empower consumers to make informed decisions that provide both growth and security.

Additionally, individuals should incorporate a diversified approach to combat inflation. Relying solely on a single product, like Infinite Banking, may not offer comprehensive protection against rising prices. Instead, a balanced portfolio that includes various assets, such as cash value life insurance, stocks, and real estate, can create a more robust strategy for enduring inflationary pressures while capitalizing on potential growth.

The Future of Financial Strategies in an Inflationary Economy

Looking ahead, the importance of adaptive financial strategies in an inflationary economy cannot be overstated. As economic conditions evolve, individuals must remain flexible and willing to adjust their financial plans to mitigate risks associated with inflation. This adaptability can involve reevaluating existing insurance policies, exploring new investment opportunities, and continuously monitoring economic indicators.

Furthermore, education about financial products and their implications for inflation is crucial. By understanding how different assets interact with inflation, consumers can better position themselves to navigate uncertainty and protect their financial future. Engaging with financial advisors who are knowledgeable about inflation hedging strategies can also provide valuable insights and help tailor personalized strategies that align with individual circumstances.

Building a Holistic Approach to Financial Security

A holistic approach to financial security involves integrating various components of financial planning, including insurance products, investment strategies, and savings plans. As inflation remains a concern, individuals should prioritize building a comprehensive financial framework that accounts for potential economic fluctuations. This approach not only secures current assets but also positions individuals for future growth.

Moreover, understanding the interplay between different financial products is essential for creating a resilient financial plan. For instance, combining cash value life insurance with other investment vehicles can enhance overall returns while providing a safety net during inflationary periods. Individuals who adopt a well-rounded financial strategy are more likely to withstand economic challenges and achieve long-term financial success.

Frequently Asked Questions

How does Infinite Banking relate to inflation hedging strategies?

Infinite Banking utilizes whole life insurance policies to create a personal banking system, allowing policyholders to access cash value and borrow against it. This approach can serve as an inflation hedging strategy by providing a source of liquidity during inflationary periods, especially as cash value accumulates at rates that may outpace inflation.

Can whole life insurance benefits protect against inflation?

Yes, whole life insurance benefits can protect against inflation. The cash value within whole life policies typically grows at a rate that exceeds inflation, providing a stable financial resource. Additionally, the death benefit remains intact, ensuring that beneficiaries receive a value that retains purchasing power over time.

What is the impact of inflation on universal life insurance policies?

Universal life insurance policies may experience impacts from inflation, particularly concerning the cash value and interest rates. However, they can still act as a hedge against inflation if the credited interest rates on cash values rise in response to market inflation, making them a viable option for financial planning during inflationary periods.

How does cash value life insurance function as an inflation hedge?

Cash value life insurance functions as an inflation hedge by accumulating value over time, which can be accessed through loans or withdrawals. This liquidity allows policyholders to navigate economic fluctuations and invest in opportunities that may arise during high inflation, thus preserving their purchasing power.

Is Infinite Banking a viable financial planning strategy during inflation?

While Infinite Banking is not uniquely designed to combat inflation, it offers some benefits during inflationary times. The cash value of whole life insurance policies can grow at rates that counter inflation, and policyholders can utilize these funds for investments. However, relying solely on Infinite Banking without considering other financial strategies may not provide complete protection against inflation.

What are the risks of using non-direct recognition loans in Infinite Banking during inflation?

Using non-direct recognition loans in Infinite Banking during inflation can pose risks such as higher borrowing costs. As inflation rises, interest rates on loans may increase, which could outpace any growth in dividend rates from the policy. This could lead to a situation where the cost of borrowing becomes more expensive without corresponding benefits in cash value growth.

Can cash value life insurance outperform inflation over time?

Yes, cash value life insurance has the potential to outperform inflation over time. Historically, the cash value in whole life and universal life policies has been designed to grow consistently, often at rates that exceed inflation, making them a suitable long-term financial tool for preserving wealth.

| Key Points | Details |

|---|---|

| Understanding Inflation | Inflation is rising, but it is predicted to be temporary, lasting 12-24 months. |

| Critique of Government Actions | The author dismisses the notion that the government manipulates inflation metrics and emphasizes the need for personal strategies rather than complaining. |

| Infinite Banking Overview | Infinite Banking alone does not provide a unique solution to combat inflation, but cash value life insurance can act as a hedge. |

| Whole Life vs. Universal Life Insurance | Both types of insurance can hedge against inflation, offering higher rates of return than traditional savings. |

| Cash Value Benefits | Cash value in life insurance policies tends to outpace inflation and can provide liquidity during economic hardship. |

| Conclusion on Infinite Banking and Inflation | While Infinite Banking has its merits, it is not uniquely positioned to combat inflation effectively. |

Summary

Infinite Banking and Inflation are interconnected topics that highlight the challenges individuals face during periods of rising prices. While proponents of Infinite Banking argue its merits in combating inflation, the reality is that traditional whole life and universal life insurance products provide a more reliable hedge against inflation. These insurance policies have historically outperformed inflation rates and offer liquidity and security during volatile economic times. Therefore, while Infinite Banking presents a strategy for personal finance, individuals should consider various financial instruments to effectively protect themselves from the effects of inflation.